Four Things to Consider Before Refinancing Your Home

Mortgage refinancing applications surged in the second week of March 2020, jumping by 79% — the largest weekly increase since November 2008. As a result, the Mortgage Bankers Association nearly doubled its 2020 refinance originations forecast to $1.2 trillion, the strongest refinance volume since 2012.1

Low mortgage interest rates have prompted many homeowners to think about refinancing, but there's a lot to consider before filling out a loan application.

1. What is your goal?

Determine why you want to refinance. Is it primarily to reduce your monthly payments? Do you want to shorten your loan term to save interest and possibly pay off your mortgage earlier? Are you interested in refinancing from one type of mortgage to another (e.g., from an adjustable-rate mortgage to a fixed-rate mortgage)? Answering these questions will help you determine whether refinancing makes sense and which type of loan might best suit your needs.

2. When should you refinance?

A general guideline is not to refinance unless interest rates are at least 2% lower than the rate on your current mortgage. However, even a 1% to 1.5% differential may be worthwhile to some homeowners.

To determine this, you should factor in the length of time you plan to stay in your current home, the costs associated with a new loan, and the amount of equity you have in your home. Calculate your break-even point (when you'll begin to save money after paying fees for closing costs). Ideally, you should be able to recover your refinancing costs within one year or less.

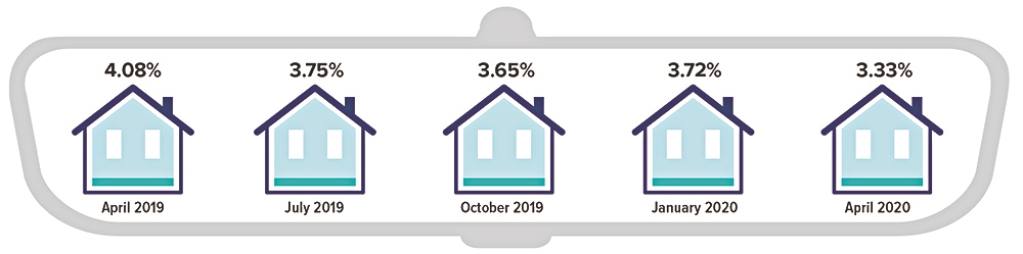

Rear-View Look at Mortgage Rates

In a single year, the average rate for a 30-year mortgage fell by 0.75%. Low mortgage interest rates often prompt homeowners to refinance.

Source: Freddie Mac, 2020 (data as of first week of April 2020)

While refinancing a 30-year mortgage may reduce your monthly payments, it will start a new 30-year period and may increase the total amount you must pay off (factoring in what you have paid on your current loan). On the other hand, refinancing from a 30-year to 15-year loan may increase monthly payments but can greatly reduce the amount you pay over the life of the loan.

3. What are the costs?

Refinancing can often save you money over the life of your mortgage loan, but this savings can come at a price. Generally, you'll need to pay up-front fees. Typical costs include the application fee, appraisal fee, credit report fee, attorney/legal fees, loan origination fee, survey costs, taxes, title search, and title insurance. Some loans may have a prepayment penalty if you pay off your loan early.

4. What are the steps in the process?

Start by checking your credit score and history. Just as you needed to get approval for your original home loan, you'll need to qualify for a refinance. A higher credit score may lead to a better refinance rate.

Next, shop around. Compare interest rates, loan terms, and refinancing costs offered by multiple lenders to make sure you're getting the best deal. Once you've chosen a lender, you will submit financial documents (such as tax returns, bank statements, and proof of homeowners insurance) and fill out an application. You may also be asked for additional documentation or a home appraisal.

1) Mortgage Bankers Association, March 11, 2020

This content is developed from sources believed to be providing accurate information. Individuals involved in the estate planning process should work with an estate planning team, including their own personal legal or tax counsel. This material has been prepared by a third party that is unaffiliated with Townsend Asset Management Corp. and is provided for informational purposes only. It may not represent the views of Townsend or its affiliates. Townsend has obtained permission to distribute this material. Townsend Asset Management Corp. is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about the firm can be found in its Form ADV Part 2, which is available upon request. TAM-20-75.